Make sure you sign up for updates as news and markets develop!

Analysts, Institutions, and Insiders Draw a Line in the Sand for NTHI

When seismic shifts happen, an earthquake is coming. A powerful swarm of analysts has just stormed into NeOnc Technologies (NASDAQ: NTHI), delivering 3 Strong Buy / Buy ratings with zero Holds or Sells.

Price targets range from $13 to $20, $16 average, pointing to massive 220%+ upside from $5, or less.

Strong confirmation of clinical activity could ignite explosive upside — rapid repricing, fresh institutional buying, analyst target hikes, and partnership rumors that send the stock soaring.

On the flip side, any disappointment could trigger a sharp, classic biotech selloff.

This is pure binary fireworks: one catalyst could dramatically reshape the entire story in either direction, it's the true definition of an explosive situation.

History shows just how explosive these Phase 2 cancer readouts can be. In recent cycles, positive efficacy signals in high-unmet-need oncology areas have triggered massive repricings:

- Monopar Therapeutics (MNPR) surged over 1,000% in 2024 on strong mucositis data momentum

- Summit Therapeutics (SMMT) jumped 576% in 2024 after standout ivonescimab lung cancer results

- Other names like certain pancreatic/ovarian cancer plays have delivered 100–500%+ gains in days to weeks on confirmatory Phase 2 data

A clean NEO100 hit in brain cancer, where options are desperately limited, could spark similar momentum as the market suddenly prices in platform validation, accelerated approval potential, and big-pharma interest.

Strong insider conviction is backed by Wall Street firepower: Chairman & CEO Amir Heshmatpour has purchased over $500K on recent open-market buys (approaching $1 million total), while institutions like Bank of America, State Street, and Barclays continue building positions. The company also looks ready to raise serious capital to push its lead programs into pivotal trials.

There are speculative biotech stories… and then there are platform stories capable of fundamentally changing treatment paradigms in areas where medicine has repeatedly failed.

NeOnc Technologies (NASDAQ: NTHI) is positioning itself firmly in the second category.

The company isn't just developing another oncology drug. It is attacking one of the toughest problems in all of cancer: delivering therapeutics across the blood-brain barrier into deadly brain tumors and the market is starting to take notice.

BBB has historically limited the effectiveness of otherwise promising therapies for glioblastoma, aggressive gliomas, pediatric CNS cancers, and metastatic brain tumors. Brain cancer remains one of oncology's deadliest and most underserved categories, because systemic therapies often cannot achieve sufficient intracranial drug concentrations without unacceptable toxicity.

NeOnc's investment case centers on the idea that delivery, not necessarily discovery alone, may be the bottleneck that has prevented meaningful therapeutic advances in CNS oncology.

Multiple converging catalysts are now drawing institutional and retail attention to NTHI.

I'm the editor of 24/7 Market News and have covered the markets for over a quarter century. During that span I've become notorious for creating very long investor theses, to describe companies, their business models, and/or the target market opportunities.

Investment Snapshot

Addressable Market

- Brain Cancer / CNS Tumors: $4.8B – $6.6B+ by 2033

- Glioblastoma (lead indication): $3B – $4B today, growing strongly

- Platform potential across multiple CNS cancers (glioma, meningioma, pediatric, metastases)

Key Catalysts (2026–2028)

Major Risks

- Binary Phase 2 data outcome (success = explosive upside, miss = sharp selloff)

- Additional capital raises / dilution

- Regulatory delays or larger Phase 3 requirement

- Competition in glioblastoma space

- Manufacturing and commercial execution

Regulatory Milestones: Fast Track designation already in place — positive data could lead to Breakthrough Therapy or RMAT designation.

Commercial Launch / Revenue: First approved product → royalty deals, upfront payments, or full commercialization.

Potential Catalysts

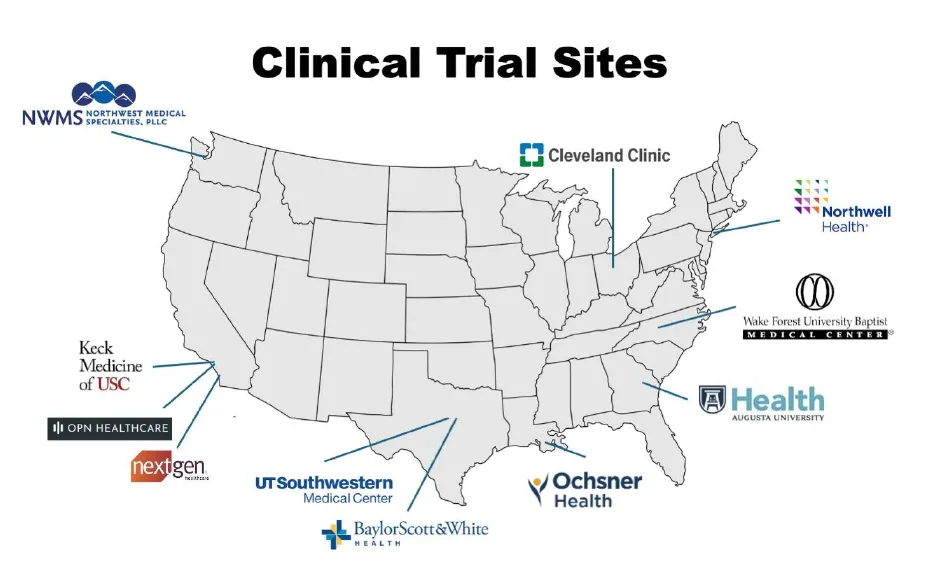

Near-term (2026): Positive interim / top-line data from NEO100 Phase 2a (recurrent IDH1-mutant high-grade glioma) — expected ~August 2026. Strong response rate / PFS6 could trigger analyst upgrades, institutional buying, and stock re-rating.

Mid-term (2026–2027): FDA End-of-Phase 2 meeting → potential accelerated approval pathway or pivotal Phase 3 design for NEO100 or NEO212.

Partnership / M&A: Big Pharma interest in BBB-delivery platform (intranasal NEO100 + NEO212 conjugate). Possible $50M+ strategic deals (e.g., Quazar-type partnerships already discussed).

Label Expansion: Success in lead indication unlocks NEO100-02 (meningioma), NEO100-03 (pediatric), and broader CNS metastases.

Bottom Line: High-risk / high-reward BBB-delivery platform play. Positive data could transform NTHI into a major CNS oncology contender.

Why Investors are Suddenly Watching NTHI

The market has increasingly started to notice four major developments simultaneously occurring:

Heavy Insider Buying

CEO and Executive Chairman Amir Heshmatpour reportedly purchased more than $500K worth of NTHI in recent weeks, bringing cumulative insider purchases close to $1M over the past year.

Open-market insider buying of this magnitude, particularly ahead of major clinical readouts, is often interpreted by biotech investors as one of the key confidence signals management can send.

Importantly, these were not option exercises or compensation grants. They were discretionary market purchases made ahead of potentially company-defining data. That timing matters.

Multiple Wall Street Initiations

Within a relatively short period, 3 separate Wall St firms initiated bullish coverage on NTHI:

Separately, Stonegate Capital Partners published a valuation range of approximately $19–$28 with a midpoint valuation of $23.04 based on a probability-adjusted DCF model.

For a clinical-stage company with a market capitalization that has recently hovered near ~$200 million, those valuation targets imply the market may still be underpricing the platform opportunity if clinical validation materializes.

Institutional Accumulation

Institutional ownership has reportedly expanded through firms including:

The combination of institutional positioning, insider buying, and expanding analyst coverage often precedes broader market discovery in emerging biotech names.

Multiple Near-Term Catalysts

This is where the story becomes especially interesting. NeOnc is approaching several meaningful clinical and strategic milestones:

- NEO100-01 Phase 2a topline data

- NEO212 Phase 2 advancement

- Potential FDA accelerated approval framework discussions

- Potential closing/funding of the proposed $50 million Quazar strategic partnership

- Expansion into pediatric brain tumors and metastatic CNS disease

- Continued AI/3D bioprinting platform development

In speculative biotech investing, timing matters almost as much as science. NTHI is entering what many investors would consider a classic "inflection-point window."

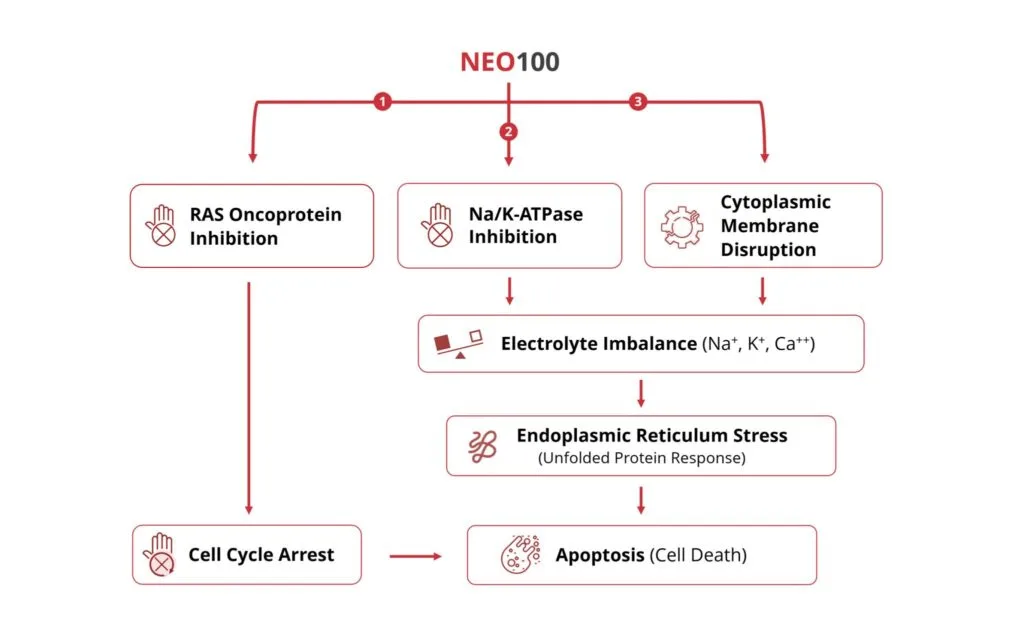

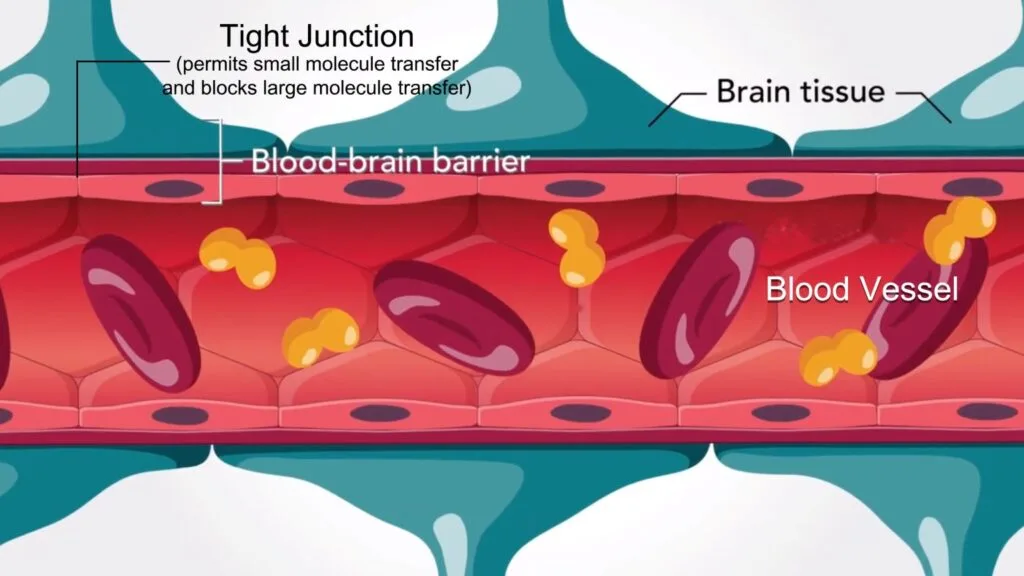

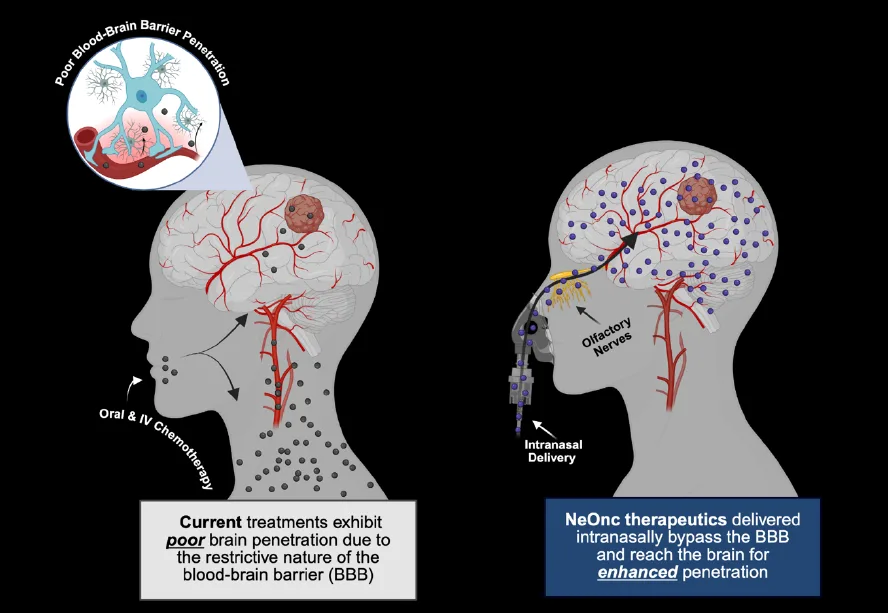

Solving the Blood-Brain Barrier Problem

The blood-brain barrier exists for a good reason: it protects the brain from toxins. Unfortunately, it also blocks many cancer therapies.

That creates a major problem in CNS oncology because drugs that may work elsewhere in the body frequently fail to reach therapeutic concentrations in brain tissue.

NeOnc's platform attempts to address this problem through two core approaches:

NEO100: Intranasal Brain Delivery

NEO100 is an intranasal therapy derived from perillyl alcohol (POH), administered through a nasal delivery system designed to bypass traditional BBB limitations through olfactory and trigeminal nerve pathways.

The strategic implications are significant:

- Non-invasive administration

- Potential at-home treatment

- Avoidance of first-pass metabolism

- Direct CNS access

- Lower systemic toxicity potential

- Scalability across multiple CNS indications

In recurrent high-grade glioma patients, NeOnc has reported:

Those numbers compare favorably against historical salvage benchmarks cited by the company in heavily pretreated populations. Importantly, tolerability has remained favorable with limited significant toxicity signals reported thus far.

That combination — potential efficacy plus manageable toxicity — is exactly what neuro-oncology investors look for.

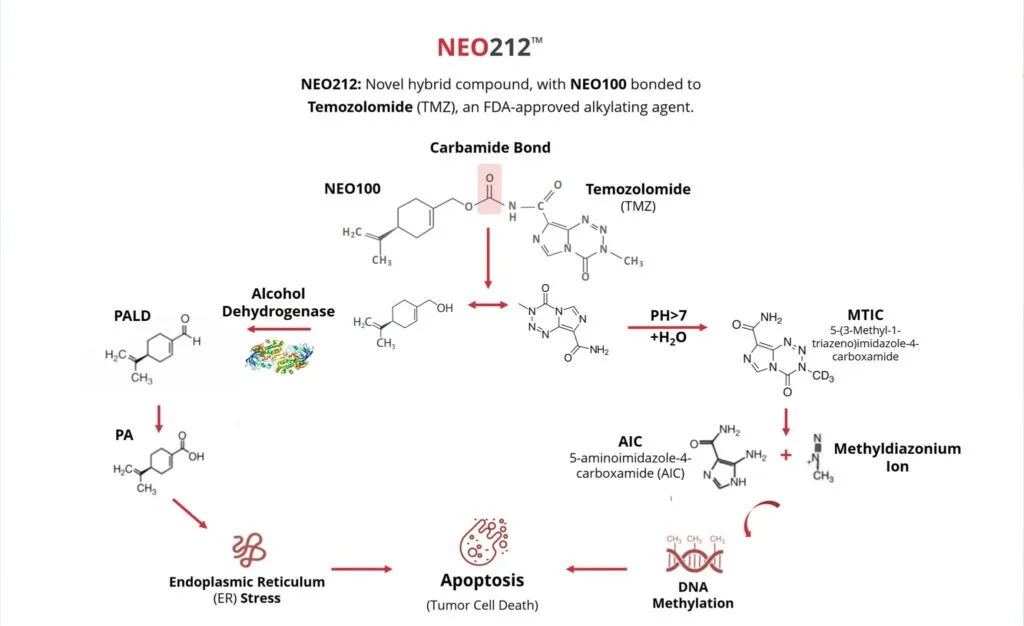

NEO212: Potentially the Bigger Opportunity

NEO212 may ultimately represent the larger commercial opportunity. NEO212 is essentially a next-generation evolution of temozolomide (TMZ), the current backbone chemotherapy used across glioblastoma treatment. But NeOnc believes it may have engineered a significantly improved version.

According to BTIG's research coverage:

- NEO212 achieves roughly 3X CNS uptake versus TMZ

- The compound may overcome MGMT-mediated resistance

- Early Phase 1 observations showed signs of antitumor activity

- Safety signals thus far appear favorable relative to conventional TMZ

That matters because temozolomide remains a multi-billion-dollar standard-of-care market despite its limitations. If NEO212 demonstrates materially improved CNS penetration and efficacy while maintaining acceptable toxicity, the addressable market opportunity could become very large very quickly.

BTIG specifically described NEO212 as potentially "reduced-risk" because it builds upon a known mechanism rather than introducing an entirely unproven therapeutic class.

Why the Platform Potential Matters

The real bull case is not just one drug. It is the possibility that Perillyl Alcohol (POH)-enabled CNS delivery becomes a broader platform capable of transporting multiple therapeutic payloads into the brain.

That could potentially expand NeOnc beyond current indications through:

- Non-invasive administration

- Potential at-home treatment

- Avoidance of first-pass metabolism

- Direct CNS access

- Lower systemic toxicity potential

- Scalability across multiple CNS indications

BTIG noted that nearly 50% of CNS-targeting compounds fail due to poor BBB penetration. If NeOnc's platform demonstrates consistent BBB transport capability, partnership interest could eventually extend beyond oncology itself and investors are increasingly paying attention.

AI, 3D Bioprinting, and Focused Ultrasound add Optionality

NeOnc has also begun integrating:

- AI-driven drug modeling

- 3D bioprinted tumor organoids

- Focused ultrasound enhancement strategies

While these programs are still early-stage, they introduce additional strategic optionality. The company described preclinical work suggesting focused ultrasound may further amplify NEO100 potency across multiple CNS tumor types. If validated clinically, this could broaden both therapeutic applicability and partnership potential.

The Market Opportunity Is Massive

The commercial backdrop is difficult to ignore. According to industry data cited in research coverage:

- ~1 million Americans live with primary brain tumors

- ~94,000 new primary brain tumors are diagnosed annually

- ~19,000 annual deaths occur from malignant brain tumors in the U.S.

- Brain metastases may affect up to hundreds of thousands of patients annually

Meanwhile, CNS oncology remains one of the most underpenetrated and difficult therapeutic markets in medicine. Even incremental survival improvements in recurrent glioblastoma can command substantial clinical and commercial value — and therapies that improve survival while reducing systemic toxicity often see significant physician adoption in fragile neuro-oncology populations.

Why the Setup Is Attractive to Speculative Biotech Investors

The Setup

- Small-cap valuation

- Underfollowed platform

- Multiple analyst initiations

- Insider accumulation

- Institutional positioning

- Near-term catalysts

- High unmet medical need

- Large TAM

- Potential platform scalability

The Trigger

Clinical data.

Everything now hinges on whether the upcoming datasets validate the platform. Positive data could materially rerate NTHI and could validate the broader BBB delivery thesis. That is the distinction investors are increasingly focused on.

The Risks

Biotech investing carries risks, including:

- Clinical trial failure

- Small dataset overinterpretation

- Regulatory delays

- Financing dilution

- Manufacturing/CMC complications

- Competitive CNS oncology landscape

- Drug-device regulatory complexity

- Failure to replicate early efficacy signals in larger studies

As repeated, brain cancer has historically been one of the hardest therapeutic categories in medicine and many promising approaches have failed. Investors should understand that clearly.

Investment / Trading Thesis

Bull Thesis

If NeOnc validates improved CNS drug delivery through either NEO100 or NEO212, NTHI could transition from a speculative microcap into a recognized CNS oncology platform leader.

The valuation disconnect becomes particularly interesting when compared against:

- Analyst PTs ranging from $13–$28

- A current market cap still near early-stage biotech levels

- Multi-billion-dollar CNS oncology markets

- Potential platform licensing optionality

NEO212 may ultimately become the primary institutional driver because it directly improves on an established standard-of-care chemotherapy already widely used in brain cancer treatment, while NEO100 provides earlier clinical validation for the broader intranasal delivery concept. Together, they create a layered platform narrative rather than a single-asset story.

Trading Thesis

NTHI appears positioned as a catalyst-driven biotech momentum setup heading into:

- Phase 2a topline data

- FDA pathway discussions

- Partnership developments

- Additional clinical updates through 2026

Historically, small-cap biotech stocks entering major CNS oncology readout windows can experience substantial volatility as investors reposition ahead of binary outcomes.

The combination of insider buying, increasing Wall Street coverage, institutional accumulation, and upcoming data catalysts — for traders, momentum likely remains heavily tied to news flow and clinical milestones.

For long-term investors, the core question is whether NeOnc can prove the BBB delivery platform works consistently and reproducibly at scale. If it can, the upside scenario becomes significantly larger than NTHI's current valuation — and recent insider activity suggests management appears willing to personally bet on that outcome.